This article was originally published on CUInsight. Read the full article here.

For decades, credit unions have navigated waves of change, adjusting to economic shifts, new regulations, and emerging technology. Those that embraced innovation didn’t just survive-they grew stronger and remained competitive.

Over the past 20 years, credit unions have moved from basic data awareness to fully integrating artificial intelligence. Each phase in this transformation has been crucial. Now, as AI reshapes financial services, credit unions must decide how they will adapt to this next major shift.

Mergers, acquisitions, and the pressure to evolve

The number of credit unions in the U.S. has declined significantly. In 1995, there were over 12,595 federally insured credit unions. By Q3 of 2023, that number had dropped below 4,645 according to data from the National Credit Union Administration (NCUA). Many merged to stay competitive, while others struggled to keep up with growing operational demands and the rise of digital banking.

Despite these challenges, credit unions that embraced technology thrived. Those that used data to improve member experiences, streamline operations, and strengthen risk management positioned themselves for long-term success.

The first shift: Data as a strategic asset (2008-2012)

The 2008 financial crisis forced credit unions to rethink how they managed risk and made decisions. During this period, data emerged as more than just a record of transactions-it became a tool for strategic growth.

A 2010 NCUA report highlighted the growing need for data-driven decision-making. Credit unions started implementing basic data collection systems to understand member behaviors and financial trends. However, many still lacked the technology to analyze and apply these insights effectively. While this period laid the foundation for data-driven operations, there was still a long road ahead.

From information to action (2013-2015)

As digital banking gained traction, member expectations evolved. Credit unions began using data analytics to enhance services, leading to more personalized interactions and improved operational efficiency.

Reports from McKinsey & Company during this period emphasized the competitive advantage of data-driven strategies. Credit unions started investing in tools that analyzed member behavior, allowing them to provide more targeted financial products. This marked the shift from simply collecting data to actively using it for better decision-making and service improvements.

The rise of predictive analytics (2016-2021)

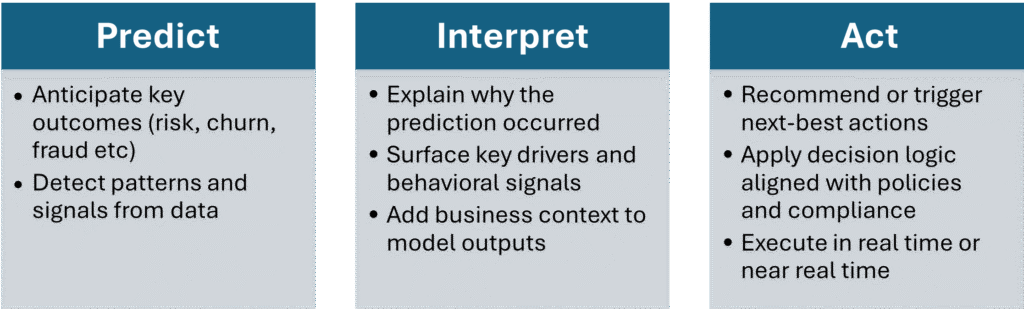

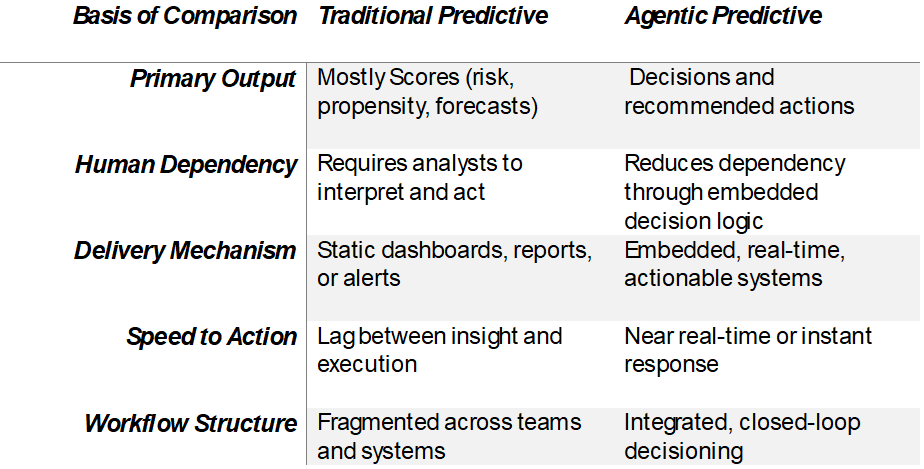

By the mid-2010s, credit unions moved beyond analyzing past trends and began using predictive models to anticipate future needs. This shift helped them enhance member experiences, detect fraud faster, and improve lending decisions.

It was observed that credit unions leveraging predictive analytics saw improved member retention and risk management. Instead of reacting to financial events as they happened, credit unions started forecasting trends, allowing them to offer proactive financial solutions tailored to members’ needs.

AI: The defining innovation of this era (2022 and beyond)

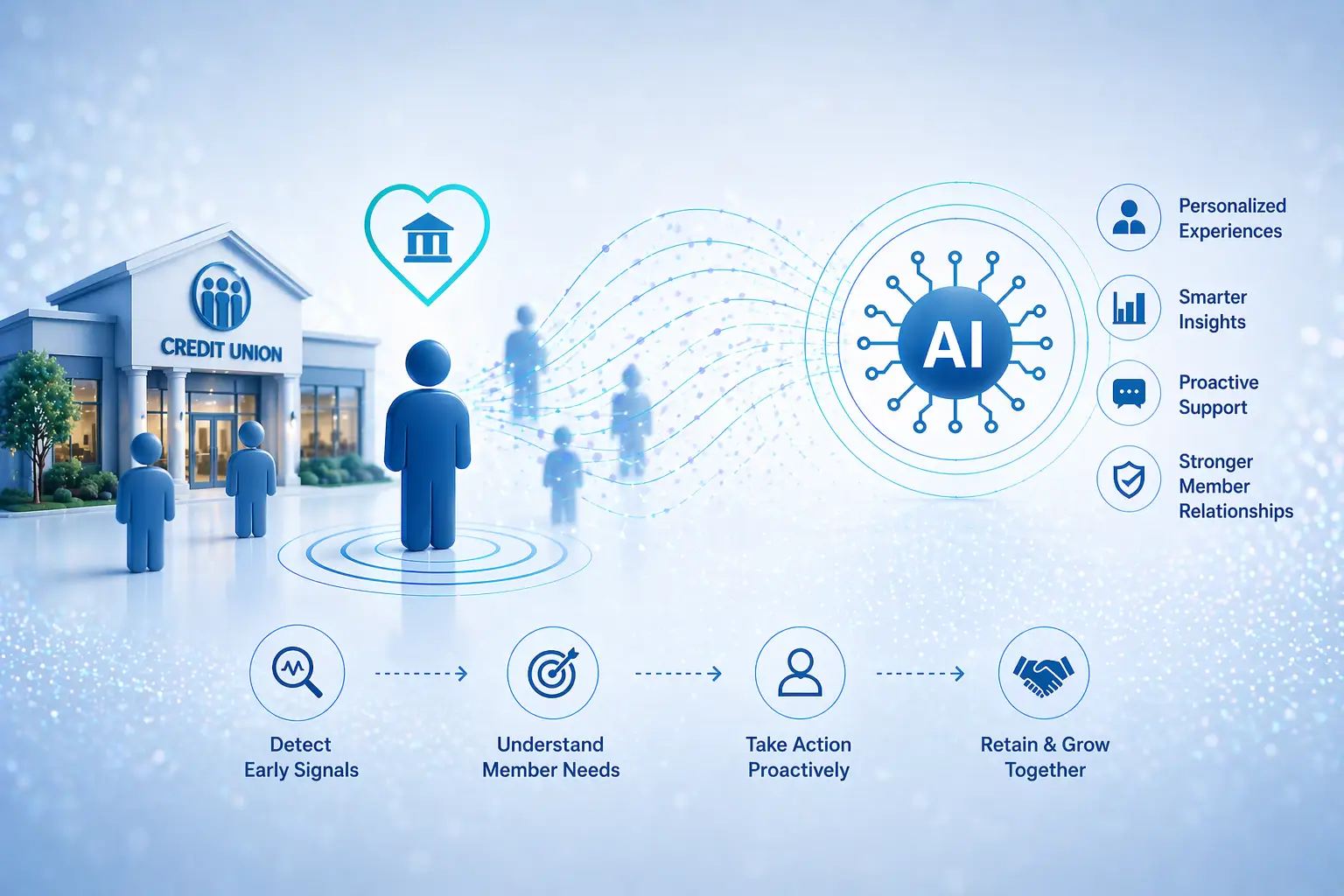

Now, credit unions are entering a new phase where artificial intelligence is transforming nearly every aspect of banking. AI is no longer an emerging concept-it is actively reshaping how credit unions interact with members, manage risk, and optimize their operations.

A 2022 Deloitte report detailed the rapid adoption of AI-driven solutions in financial services. Credit unions are already integrating AI-powered chatbots to provide 24/7 member support, using machine learning models to improve fraud detection, and leveraging AI for more precise credit risk analysis.

Hyper-personalization has also become a reality, with AI allowing credit unions to offer financial products tailored to individual member needs. Instead of relying on broad demographic trends, AI enables institutions to understand each member’s unique financial situation and provide solutions that truly add value.

Credit unions: Adapting, growing, and looking ahead

Credit unions have faced numerous challenges over the years-mergers, regulatory changes, and digital disruption. Yet, their ability to evolve has kept them relevant and strong. From the early days of data collection to predictive analytics and now AI, credit unions have consistently adapted to better serve their members.

AI is not the final step-it’s just the next chapter. As technology continues to evolve, credit unions that stay ahead of the curve will define the future of financial services. By embracing AI, they can enhance member experiences, improve efficiency, and ensure long-term growth.

At AiVantage, we are growing as a strategic AI partner for forward-looking credit unions. Contact us today to learn how we can support your journey into the AI-driven future.

For decades, credit unions have navigated waves of change, adjusting to economic shifts, new regulations, and emerging technology. Those that embraced innovation didn’t just survive-they grew stronger and remained competitive.

Over the past 20 years, credit unions have moved from basic data awareness to fully integrating artificial intelligence. Each phase in this transformation has been crucial. Now, as AI reshapes financial services, credit unions must decide how they will adapt to this next major shift.

Mergers, acquisitions, and the pressure to evolve

The number of credit unions in the U.S. has declined significantly. In 1995, there were over 12,595 federally insured credit unions. By Q3 of 2023, that number had dropped below 4,645 according to data from the National Credit Union Administration (NCUA). Many merged to stay competitive, while others struggled to keep up with growing operational demands and the rise of digital banking.

Despite these challenges, credit unions that embraced technology thrived. Those that used data to improve member experiences, streamline operations, and strengthen risk management positioned themselves for long-term success.

The first shift: Data as a strategic asset (2008-2012)

The 2008 financial crisis forced credit unions to rethink how they managed risk and made decisions. During this period, data emerged as more than just a record of transactions-it became a tool for strategic growth.

A 2010 NCUA report highlighted the growing need for data-driven decision-making. Credit unions started implementing basic data collection systems to understand member behaviors and financial trends. However, many still lacked the technology to analyze and apply these insights effectively. While this period laid the foundation for data-driven operations, there was still a long road ahead.

From information to action (2013-2015)

As digital banking gained traction, member expectations evolved. Credit unions began using data analytics to enhance services, leading to more personalized interactions and improved operational efficiency.

Reports from McKinsey & Company during this period emphasized the competitive advantage of data-driven strategies. Credit unions started investing in tools that analyzed member behavior, allowing them to provide more targeted financial products. This marked the shift from simply collecting data to actively using it for better decision-making and service improvements.

The rise of predictive analytics (2016-2021)

By the mid-2010s, credit unions moved beyond analyzing past trends and began using predictive models to anticipate future needs. This shift helped them enhance member experiences, detect fraud faster, and improve lending decisions.

It was observed that credit unions leveraging predictive analytics saw improved member retention and risk management. Instead of reacting to financial events as they happened, credit unions started forecasting trends, allowing them to offer proactive financial solutions tailored to members’ needs.

AI: The defining innovation of this era (2022 and beyond)

Now, credit unions are entering a new phase where artificial intelligence is transforming nearly every aspect of banking. AI is no longer an emerging concept-it is actively reshaping how credit unions interact with members, manage risk, and optimize their operations.

A 2022 Deloitte report detailed the rapid adoption of AI-driven solutions in financial services. Credit unions are already integrating AI-powered chatbots to provide 24/7 member support, using machine learning models to improve fraud detection, and leveraging AI for more precise credit risk analysis.

Hyper-personalization has also become a reality, with AI allowing credit unions to offer financial products tailored to individual member needs. Instead of relying on broad demographic trends, AI enables institutions to understand each member’s unique financial situation and provide solutions that truly add value.

Credit unions: Adapting, growing, and looking ahead

Credit unions have faced numerous challenges over the years-mergers, regulatory changes, and digital disruption. Yet, their ability to evolve has kept them relevant and strong. From the early days of data collection to predictive analytics and now AI, credit unions have consistently adapted to better serve their members.

AI is not the final step-it’s just the next chapter. As technology continues to evolve, credit unions that stay ahead of the curve will define the future of financial services. By embracing AI, they can enhance member experiences, improve efficiency, and ensure long-term growth.

At AiVantage, we are growing as a strategic AI partner for forward-looking credit unions. Contact us today to learn how we can support your journey into the AI-driven future.